SkillClick

SkillClick

U.S. Charging as a Service Market Outlook 2026–2033 with Key Trends and Opportunities

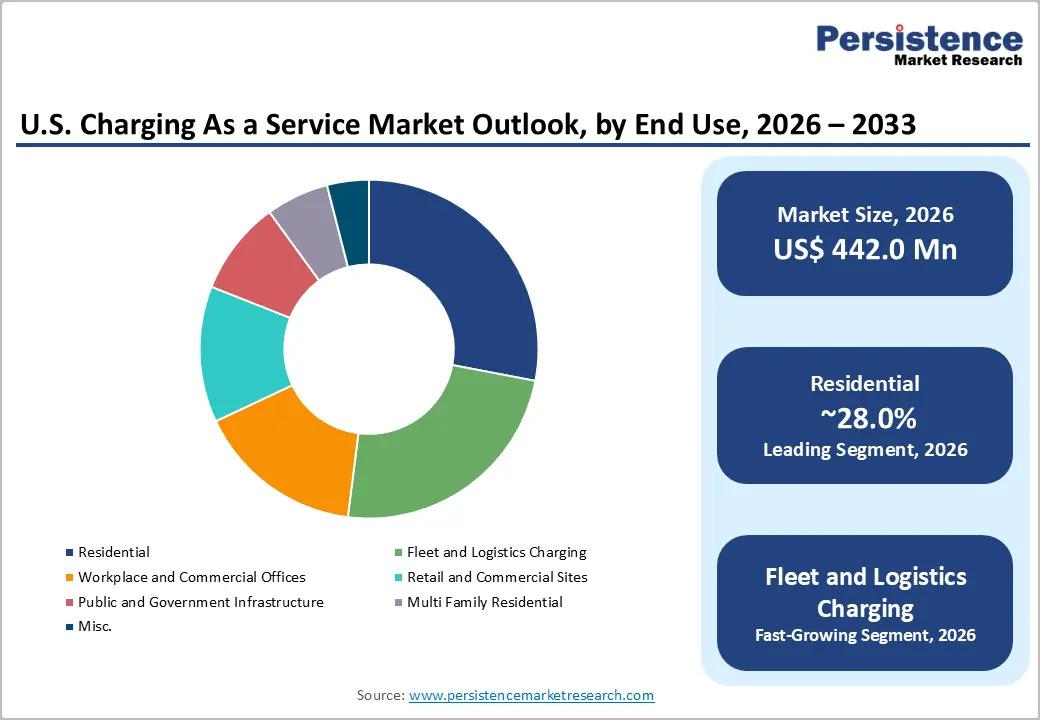

According to Persistence Market Research Insights, the U.S. Charging as a Service (CaaS) market is expected to be valued at US$ 442.0 million in 2026 and is projected to reach US$ 2,585.1 million by 2033, expanding at a remarkable CAGR of 28.7% during the forecast period. The market’s rapid expansion is driven by strong federal and state support for electric vehicle (EV) adoption, accelerating fleet electrification, and the increasing preference for subscription-based infrastructure models that eliminate large upfront investments associated with EV charging deployment.

Charging as a Service is transforming how organizations deploy and manage EV charging infrastructure. Instead of purchasing, installing, and maintaining charging systems outright, businesses, municipalities, fleet operators, and property owners can access charging solutions through service agreements that bundle equipment, software, maintenance, monitoring, and upgrades into predictable monthly payments. This model significantly reduces capital expenditure requirements while enabling scalable EV charging networks.

Market Trends

One of the most influential trends shaping the U.S. Charging as a Service market is the growing adoption of subscription-based charging infrastructure among commercial fleet operators. Companies transitioning to electric delivery vehicles, buses, and service fleets are increasingly seeking solutions that minimize financial risk and simplify infrastructure management.

Another key trend is the integration of smart charging technologies and energy management platforms. Service providers are incorporating artificial intelligence, real-time monitoring, predictive maintenance, and load-balancing capabilities to optimize charging operations and reduce energy costs. These advancements allow organizations to maximize charger utilization while ensuring reliable charging availability.

The expansion of workplace charging, multi-family residential charging, and public charging hubs is also driving demand for CaaS solutions. Property owners are leveraging service-based models to provide EV charging amenities without the burden of owning and managing charging infrastructure.

Market Drivers

Rising EV Adoption Across the United States

The rapid growth of electric vehicle ownership remains the primary driver for the Charging as a Service market. As EV sales continue to increase across passenger vehicles, commercial fleets, and public transportation systems, the need for accessible and scalable charging infrastructure becomes increasingly critical.

Businesses and municipalities are seeking cost-effective methods to support EV adoption while avoiding substantial upfront capital investments. Charging as a Service provides an attractive alternative by converting large infrastructure expenses into manageable operational costs.

Government Incentives and Policy Support

Federal and state governments continue to promote transportation electrification through grants, tax incentives, infrastructure funding programs, and emissions reduction initiatives. These programs encourage organizations to deploy EV charging infrastructure while supporting the broader transition toward sustainable mobility.

Public-sector investments in charging networks are creating favorable conditions for CaaS providers, enabling faster deployment of charging solutions across urban, suburban, and rural regions.

Fleet Electrification Initiatives

Commercial fleet operators are increasingly transitioning to electric vehicles to reduce fuel costs, comply with environmental regulations, and achieve sustainability targets. Charging as a Service enables fleet managers to deploy charging infrastructure quickly without diverting significant capital away from core business operations.

The growing adoption of electric delivery vans, logistics vehicles, school buses, and municipal fleets is expected to generate substantial demand for managed charging solutions throughout the forecast period.

Market Restraints and Challenges

Grid Infrastructure Constraints

Despite strong market growth prospects, grid capacity limitations remain a significant challenge. Large-scale EV charging deployments often require utility upgrades, transformer enhancements, and increased power availability. These requirements can extend project timelines and increase implementation costs.

Regulatory and Permitting Complexities

Charging infrastructure projects frequently involve multiple stakeholders, including utilities, local governments, property owners, and service providers. Navigating permitting requirements and regulatory approvals can delay installations and create operational challenges for market participants.

Technology Standardization Issues

The EV charging ecosystem continues to evolve rapidly, with varying charging standards, hardware requirements, and software platforms. Ensuring interoperability and future-proofing charging investments remains a concern for both providers and customers.

Market Opportunities

Expansion of Multi-Family Residential Charging

The growing number of EV owners residing in apartments and condominiums presents a significant opportunity for Charging as a Service providers. Property managers increasingly view charging infrastructure as a valuable amenity that attracts and retains tenants while enhancing property value.

Growth of Public Charging Networks

As EV adoption expands nationwide, demand for accessible public charging stations is expected to rise substantially. Charging as a Service providers can capitalize on this trend by partnering with municipalities, retailers, hospitality businesses, and transportation hubs to deploy charging infrastructure without requiring large upfront investments.

Renewable Energy Integration

The combination of EV charging infrastructure with renewable energy systems and battery storage technologies creates new opportunities for service providers. Integrated energy solutions can reduce electricity costs, improve grid resilience, and support sustainability objectives for customers.

Segmentation Analysis

By Charger Type

DC fast chargers dominate revenue generation due to their ability to support rapid charging for commercial fleets and public charging networks. These systems are increasingly deployed along highways, logistics hubs, and high-traffic locations where minimizing charging time is essential.

Level 2 chargers represent a substantial portion of installations, particularly in workplaces, residential communities, and destination charging applications where vehicles remain parked for extended periods.

By Service Type

Fully managed charging services account for the largest market share as organizations increasingly prefer comprehensive solutions that include installation, monitoring, maintenance, software management, and technical support.

Energy management and smart charging services are expected to experience the fastest growth as customers seek to optimize electricity consumption and reduce operational costs.

By End User

Commercial fleet operators constitute the leading end-user segment due to ongoing electrification initiatives across transportation and logistics sectors.

Multi-family residential properties are expected to witness significant growth as EV ownership expands among apartment and condominium residents.

Municipalities, workplaces, retail locations, and educational institutions also represent key demand centers for Charging as a Service solutions.

Regional Outlook

The United States continues to emerge as one of the most dynamic EV charging markets globally, supported by aggressive electrification targets and substantial infrastructure investments.

California remains the largest regional market due to its leadership in EV adoption, supportive regulatory environment, and extensive charging network deployment. States including Texas, Florida, New York, and Washington are also witnessing strong growth as businesses and local governments expand charging infrastructure investments.

Urban centers continue to account for the majority of charging deployments; however, increasing funding for rural charging infrastructure is expected to broaden market opportunities across underserved regions. As federal infrastructure programs accelerate charger installations nationwide, Charging as a Service providers are expected to play a crucial role in expanding charging accessibility and supporting long-term EV adoption goals.

Competitive Landscape

The U.S. Charging as a Service market is characterized by intense competition among charging network operators, energy service providers, technology firms, and infrastructure specialists. Market participants are focusing on expanding service portfolios, enhancing software capabilities, and forming strategic partnerships to strengthen their market positions.

Leading companies are investing heavily in smart charging technologies, predictive maintenance systems, and energy management platforms to deliver greater value to customers. The competitive environment is also encouraging innovation in subscription-based business models, allowing organizations to deploy charging infrastructure with minimal financial risk.

As EV adoption accelerates and infrastructure demand rises, companies offering scalable, reliable, and cost-effective Charging as a Service solutions are expected to capture significant growth opportunities throughout the forecast period.

- Managerial Effectiveness!

- Future and Predictions

- Motivatinal / Inspiring

- Fitness and Wellness

- Medical & Health

- Manufacturing

- Education

- Real-Estate

- Food Industry

- Hospitality

- Online Games

- Sports

- Home Services

- Civil Engineering

- Safety and Protection

- Software Products & Services

- Fashion and Jewellery

- Artificial Intelligence

- Entrepreneurship

- Mentoring & Guidance

- Marketing

- Networking

- HR & Recruiting

- Literature

- Shopping

- Career Management & Advancement