SkillClick

SkillClick

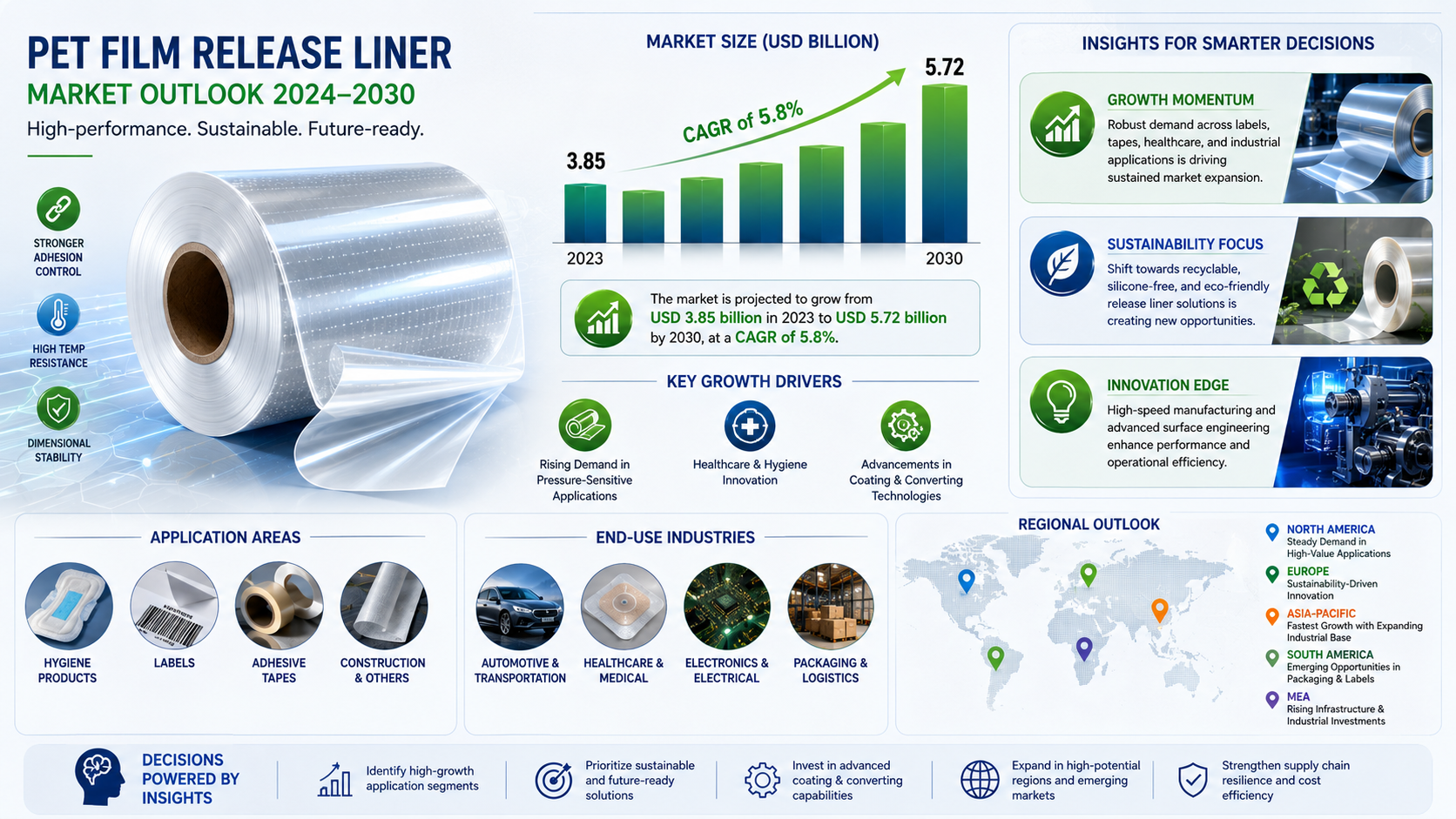

Global PET Film Release Liner Market to Reach USD 5.72 Billion by 2030, Fueled by PSA Demand, Healthcare Innovation, and Sustainable Packaging Trend

Global PET Film Release Liner market was valued at US$ 3.85 billion in 2023 and is projected to reach US$ 5.72 billion by 2030, growing at a CAGR of 5.8% during the forecast period.

PET Film Release Liners have become indispensable components in pressure-sensitive adhesive applications, offering superior dimensional stability and temperature resistance compared to traditional paper release liners. These engineered films are revolutionizing industries ranging from healthcare labels to industrial tapes, with their ability to maintain performance integrity under extreme conditions while accommodating high-speed converting processes.

Get Full Report Here: https://www.24chemicalresearch.com/reports/267032/global-pet-film-release-liner-market-2024-2030-263

Market Dynamics:

The PET Film Release Liner market exhibits a dynamic interplay between evolving end-user demands, technological advancements, and sustainability imperatives. While the market continues its upward trajectory, manufacturers must navigate complex supply chain dynamics and increasing regulatory scrutiny.

Powerful Market Drivers Propelling Expansion

-

Explosive Growth in Pressure-Sensitive Adhesives: The PSA market, projected to exceed $13 billion globally by 2025, is driving unprecedented demand for high-performance release liners. PET films dominate in applications requiring dimensional stability under varying humidity conditions, capturing over 60% of technical label applications. The shift from solvent-based to eco-friendly PSA formulations has further intensified the need for specialized PET release surfaces that maintain consistent release forces.

-

Medical and Hygiene Sector Innovations: The healthcare revolution has created rigorous demands for release liners in wound care products, transdermal patches, and surgical drapes. Medical-grade PET films must meet USP Class VI and ISO 10993 biocompatibility standards while ensuring precise adhesive transfer. Meanwhile, the hygiene industry's growth - particularly in emerging markets - requires liners that can withstand sterilization processes while preventing adhesive migration.

-

Advanced Manufacturing Capabilities: Modern converting technologies now operate at speeds exceeding 1,000 meters per minute, necessitating PET films with exceptional uniformity and surface energy consistency. Leading manufacturers have responded with proprietary silicone coating technologies that maintain release forces within ±10% tolerances across production runs, significantly reducing downstream processing issues.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/267032/global-pet-film-release-liner-market-2024-2030-263

Significant Market Restraints Challenging Adoption

While the market shows strong growth potential, several barriers must be addressed for widespread adoption across cost-sensitive applications.

-

Raw Material Volatility: PET resin prices have shown 15-25% quarterly fluctuations over the past three years, directly impacting production costs. The specialty silicone coatings used for release surfaces add an additional 30-40% to material costs compared to conventional PET films. This volatility creates pricing challenges for converters serving price-sensitive market segments.

-

Recycling Infrastructure Gaps: Despite being technically recyclable, most PET release liners end up in landfills due to contamination from adhesives and silicone residues. Current mechanical recycling yields for post-industrial waste barely reach 50%, while the lack of standardized collection systems for post-consumer liners remains a significant barrier to circular economy initiatives.

Critical Market Challenges Requiring Innovation

The industry faces pressing technical challenges that require coordinated R&D efforts across the value chain. Maintaining consistent release force in high-speed converting applications remains problematic, with variations exceeding acceptable thresholds in nearly 20% of production batches. Furthermore, achieving optimal anchorage of silicone coatings to PET substrates demands sophisticated plasma treatment or primer applications that add complexity to manufacturing processes.

The environmental impact of liner waste is becoming a critical concern. With an estimated 2.3 million metric tons of release liner waste generated annually worldwide, regulatory pressures are mounting in Europe and North America. Manufacturers are investing heavily in mono-material structures and silicone-free release technologies to address these challenges, though commercial adoption remains limited.

Vast Market Opportunities on the Horizon

-

Electronics Industry Transformation: The emergence of flexible electronics and thin-film photovoltaics presents exciting new applications for PET release liners. These markets require ultra-smooth (<1 nm Ra) surfaces that can withstand temperatures up to 200°C during device fabrication. Early adopters have demonstrated 30-40% improvements in device yields using specialized PET carrier films compared to traditional alternatives.

-

Sustainable Solutions Development: The push for circular economy solutions has led to breakthroughs in recyclable silicone chemistries and thermoplastic release coatings. A recent industry collaboration successfully demonstrated a fully recyclable PET liner system that maintains performance characteristics while enabling closed-loop recycling. Such innovations could capture a significant share of the $500 million sustainable packaging adhesives market.

-

Emerging Market Expansion: Developing economies in Southeast Asia and Africa are experiencing 8-12% annual growth in label and tape consumption, creating substantial demand for cost-effective PET liner solutions. Localized production hubs are emerging to serve these markets, leveraging regional PET resin supplies and lower manufacturing costs while meeting increasingly sophisticated application requirements.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Silicone Film and Non-Silicone Film categories. Silicone-coated PET films currently dominate, accounting for approximately 85% of the market by value. Their superior release characteristics and thermal stability make them indispensable for demanding applications like medical device manufacturing and high-temperature industrial tapes.

By Application:

Key application segments include Hygiene Products, Cosmetics, Construction, and Others. The Hygiene segment commands the largest market share, driven by relentless innovation in disposable medical products and adult incontinence solutions. The Construction segment is emerging as the fastest-growing market, with PET liners enabling next-generation adhesive solutions for building envelopes and energy-efficient windows.

By End-User Industry:

The end-user landscape spans labels, tapes, graphic arts, and specialty applications. The labels industry remains the dominant consumer, particularly for high-value applications like RFID tags and tamper-evident packaging. The tapes sector is witnessing accelerated adoption of PET liners for automotive and electronics applications where dimensional stability is critical.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/267032/global-pet-film-release-liner-market-2024-2030-263

Competitive Landscape:

The global PET Film Release Liner market features a mix of multinational material science companies and specialized film converters. The top three players - DuPont, Polyplex Corporation, and Mondi - collectively hold approximately 45% of the market share. These industry leaders differentiate themselves through proprietary coating technologies, global supply chain networks, and strong technical service capabilities.

List of Key PET Film Release Liner Companies Profiled:

-

DuPont (U.S.)

-

Tekra (U.S.)

-

Polyplex Corporation (India)

-

Infinity Tapes (U.S.)

-

Guangtai Adhesive Products (China)

-

Siliconature (Italy)

-

Fox River Associates (U.S.)

-

Newmax Tec (Taiwan)

-

CCL Label (Canada)

-

Mondi (Austria)

-

Laufeburg (Switzerland)

-

Xinfeng Group (China)

-

Fujiko (Japan)

-

Formula Corporation (South Korea)

Market participants are focusing on vertical integration strategies, with leading players investing in inline coating capabilities and proprietary silicone formulations. The competitive landscape is further characterized by strategic partnerships throughout the value chain, from resin suppliers to end-users, to co-develop application-specific solutions.

Regional Analysis: A Global Footprint with Distinct Leaders

-

Asia-Pacific: Commands 45% of global consumption, driven by China's massive label and packaging industry along with Southeast Asia's growing electronics manufacturing sector. The region benefits from integrated PET production facilities and strong government support for material science industries.

-

North America: Represents 28% of the market, characterized by high-value applications in healthcare and specialty tapes. The U.S. leads in innovative silicone coating technologies and recycling initiatives, with several pilot plants demonstrating promising results in PET liner circularity.

-

Europe: Accounts for 22% of demand, with stringent sustainability regulations driving development of bio-based PET alternatives and recyclable release systems. Germany and Italy remain innovation hubs for high-performance films serving automotive and industrial applications.

Get Full Report Here: https://www.24chemicalresearch.com/reports/267032/global-pet-film-release-liner-market-2024-2030-263

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/267032/global-pet-film-release-liner-market-2024-2030-263

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

- Managerial Effectiveness!

- Future and Predictions

- Motivatinal / Inspiring

- Fitness and Wellness

- Medical & Health

- Manufacturing

- Education

- Real-Estate

- Food Industry

- Hospitality

- Online Games

- Sports

- Home Services

- Civil Engineering

- Safety and Protection

- Software Products & Services

- Fashion and Jewellery

- Artificial Intelligence

- Entrepreneurship

- Mentoring & Guidance

- Marketing

- Networking

- HR & Recruiting

- Literature

- Shopping

- Career Management & Advancement